Lower construction growth and overcapacity affect the sector, but the outlook for 2016 has improved.

- Lower construction growth and overcapacity affect the sector

- Payments take 60 days on average

- Improved outlook for 2016

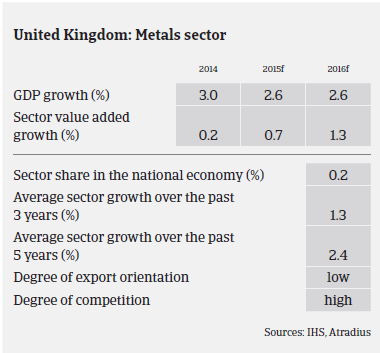

The British steel and metals industry has benefited from the UK economic rebound, but recently it has been affected by subdued performance of the construction sector, which is a main consumer of steel. Additionally, exchange rate volatility, high energy costs, competition and on-going austerity measures continue to weigh on the performance and financial strength of steel and metals businesses.

Decreased steel prices and overcapacity in the market (mainly due to the slowdown in Chinese economic growth) have impaired revenues, margins, profits and cash flow for many businesses. Consequently, in a bid to mitigate liquidity risks, cost cutting programmes and vigilant cost management strategies have been implemented and inventories are being unwound and non-core assets disposed of. However, while cost containment measures have been the industry´s main response to overcapacity so far, this could turn out to be just a short-term remedy. Maintaining margins through cost reduction and focusing on high-end products should not be seen as an ultimate solution to structural problems.

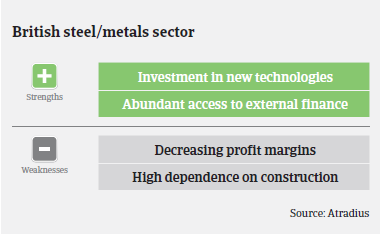

That said, many businesses have already invested in new technologies, such as laser cutting and detailed integrity scanners in order to gain competitive advantages. In the steel and metals industry the ability of businesses to process products efficiently is a major asset.

The balance sheets of steel and metals businesses are often dominated by a mixture of tangible assets in the form of property and machinery and debtor books, upon which finance can be raised. The main source of working capital funding within the sector remains invoice discounting facilities, given the nature of the debtor books. This has allowed businesses to increase their facility when and while they are growing. The UK banking sector faces increased scrutiny from the UK government to lend to businesses in an attempt to bolster economic growth. We should be mindful of the fact that many steel businesses are viable banking propositions given the profile of the asset base. The availability of liquidity within the industry has aided a rather benign insolvency development.

After a challenging start of 2015, the outlook for the British steel and metals industry for the second half of 2015 remains volatile, with on-going uncertainty arising from Eurozone austerity and further slowing of Chinese growth being constant risk factors. However, looking further ahead into early 2016, there is some optimism that sector performance will improve on the back of increasing volumes. While growth in the new housing sector has a low impact on the industry (there is low demand for steel and metals in this segment), expected growth in the non-residential building and infrastructure segments should help the sector. At this stage, access to additional financing will be key for the growth of steel and metals businesses (especially for service centres) in order to re-stock and meet the anticipated rise in demand.

The average payment duration in the UK steel and metals industry is 60 days. Despite the current challenges, payment delays are not expected to increase for the time being. Insolvencies are not expected to increase in 2015, as the volume of UK steel consumption is still rising. However, caution is advised due to the still fragile nature of the sector, which can lead to unexpected failures.

Our underwriting approach remains selective, as market conditions are unstable and the potential volatility of a rebound should not be underestimated. However, we continue to underwrite positively on acceptable risks. While our underwriting strategy is largely on a case-by-case basis, over the last few years, we have adopted a comprehensive understanding of the sector and the prevailing issues. As such, we have further developed relationships with many of the buyers in our portfolio, allowing us to obtain non-publicly available information in order to review current commitments as well as to consider new limit applications on a fully informed basis. The role of credit insurance within the industry has a long-standing history and, as such, the value of credit insurance is well respected.

Related documents

1010KB PDF